View of the Phoenix Medical Office Market

Leasing Activity

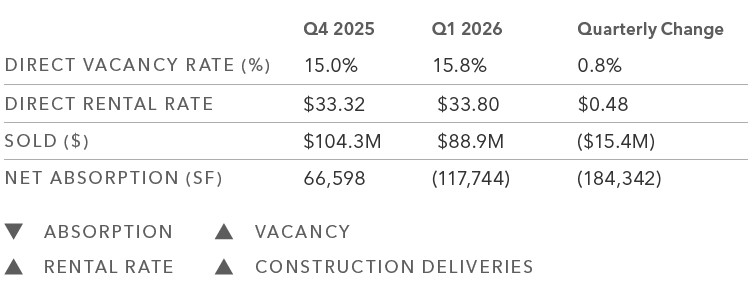

Direct vacancy increased slightly in Q1 2026, rising to 15.8% from 15.0% last quarter. This marks a shift after several quarters of gradual tightening. Even with that change, average direct rental rates moved higher, increasing to $33.80/SF from $33.32/SF on a full-service basis, which underscores that top-tier medical space is still achieving strong pricing. Leasing momentum softened as net absorption turned negative at (117,744) SF, reversing the 66,598 SF of positive absorption recorded in Q4. We are seeing longer decision timelines and fewer large space requirements as tenants adjust to higher operating costs. Construction costs remain elevated, but we continue to see more creative deal structures and negotiated solutions as groups work through today’s cost environment.

Sales Activity

Sales volume eased in Q1 2026, declining to $88.9 million from $104.3 million in Q4. Buyer interest remains, but financing standards continue to shape pricing and transaction velocity. Lenders have held firm on underwriting, which has kept some deals from penciling at seller expectations. That said, notable trades, including the approximately $30 million transaction at 21250 W Roosevelt Street in Buckeye, confirm that capital is still active for well-positioned assets. The market remains bifurcated: opportunities priced to today’s conditions, particularly those sourced off-market or positioned thoughtfully, continue to trade, while aggressively priced listings can sit for extended periods.

Construction

Development remains limited in Q1 2026. High construction costs, paired with direct vacancy rising to 15.8%, continue to reduce speculative starts and keep many projects in planning longer than normal. Even so, select projects are moving forward where demand is clear and health system sponsorship supports execution. Office-to-medical conversions continue to add supply across the Valley’s approximately 17.0 million square feet of medical office inventory, offering a more efficient path to new space in certain submarkets. With absorption turning negative this quarter, we expect new supply decisions to stay disciplined—targeted to proven demand, strong locations, and credit-backed tenancy.

Market Breakdown

Read the full report at the link below.

The information in this update was composed by the Kidder Mathews Phoenix healthcare brokerage team of Michael Dupuy, Fletcher Perry, Rachael Thompson, Perry Gabuzzi, Chad Sutton, and Zack Harris.

Data source: CoStar

About the Team

The Kidder Mathews team of Michael Dupuy, Fletcher Perry, Rachael Thompson, Perry Gabuzzi, Chad Sutton, and Zack Harris specializes in healthcare real estate services with a strategic focus on the greater Phoenix region. For more information, visit their online team profile here.

About Kidder Mathews

Kidder Mathews is the largest fully independent commercial real estate firm in the Western U.S., with over 900 professionals in 19 offices across Washington, Oregon, California, Nevada, and Arizona. We offer a complete range of brokerage, appraisal, asset services, consulting, and debt & equity finance services for all property types. For more information, visit kidder.com.

Contact

Michael Dupuy, Executive Vice President

Fletcher Perry, Executive Vice President

Rachael Thompson, Senior Vice President

Perry Gabuzzi, Senior Vice President

Chad Sutton, Associate

Zack Harris, Associate

Stay in the know and subscribe to our monthly Western U.S. Market Trends report and our quarterly market research.