A port terminal lease is rarely just a rent negotiation.

Unlike a conventional industrial lease, a port terminal depends on the performance of an entire operating platform: land, berths, cranes, rail access, truck gates, utilities, security, technology, labor, machinery and equipment, public funding, and long-term capital planning. If those elements are not aligned, even a strategically located terminal can face meaningful operating risk.

That is what makes port terminals a compelling example of real estate “beyond the core four” (industrial, retail, multifamily, and office). From a distance, they may look like industrial land. In practice, their value is tied to throughput, infrastructure control, equipment reliability, public approvals, customer commitments, and the ability to move freight safely, efficiently, and competitively.

When a port terminal lease comes up for renewal, the question should not be limited to rent per acre. The more important question is whether the lease reflects how the terminal actually functions: what infrastructure is required, who controls it, who maintains it, who funds modernization, and who bears the risk if public infrastructure does not perform.

For owner-users, terminal operators, port authorities, attorneys, lenders, investors, accountants, and public agencies, port terminal lease negotiations require specialized analysis. Comparable rent is only one part of the equation. The more complete analysis connects lease economics to infrastructure performance, machinery and equipment, capital obligations, public-private risk allocation, and long-term operating utility.

Why Are Port Terminal Leases Different from Conventional Industrial Leases?

Industrial port terminals sit at the intersection of real estate, public infrastructure, transportation, labor, environmental policy, and capital investment. They generate significant economic activity, support regional employment, and play a critical role in supply chain reliability. They also create operational and community impacts, including truck traffic, emissions, noise, security restrictions, land-use constraints, and environmental justice considerations.

Port terminals also depend on specialized labor: longshore workers, equipment operators, mechanics, truck drivers, warehouse workers, rail crews, security personnel, maintenance contractors, technology vendors, customs brokers, and freight forwarders, along with the regional service businesses that support them. Because of that, a lease structure that ignores terminal functionality can affect far more than the landlord and tenant. It can influence working hours, vessel schedules, truck congestion, rail utilization, repair cycles, and the ability of regional businesses to receive and move goods.

The scale of the public interest is measurable. Public-source data from the American Association of Port Authorities indicates that port and maritime activity supports millions of jobs and nearly three trillion dollars of United States gross domestic product. The United States Maritime Administration identifies hundreds of United States ports and a daily flow of cargo imports measured in millions of tons. Those figures are national indicators, not terminal-specific data, but they frame the magnitude of what is at stake when waterfront infrastructure is leased and operated.

This makes the public interest unavoidable. A port terminal lease may appear to be a private negotiation between landlord and tenant, but in many cases, it is also a public-policy decision about how limited waterfront infrastructure should be used.

Port authorities must balance cargo efficiency with clean-air goals, infrastructure investment, community concerns, tourism priorities, recreational marine uses, resilience planning, and public finance obligations. Terminal operators, meanwhile, need sufficient control over the assets and infrastructure required to meet customer commitments and operate efficiently.

Those interests do not always move in the same direction.

A port may want higher rent, expanded throughput, cleaner equipment, public-facing improvements, or a more flexible capital plan. A terminal operator may need berth certainty, reliable cranes, rail access, gate capacity, utility upgrades, equipment modernization, and protection for tenant-funded capital. When those issues are not addressed directly, the lease can become a rent dispute wrapped around an infrastructure problem.

How Does Public Infrastructure Affect Port Terminal Lease Economics?

A public port authority is often more than a landlord. Depending on the market and asset, it may own or control the land, wharf, berth, roads, utilities, rail interface, security infrastructure, terminal facilities, cranes, passenger facilities, or other capital assets. It may also influence tariff rules, access protocols, harbor planning, environmental commitments, bond financing, grant applications, tenant selection, and public messaging.

That makes the negotiation fundamentally different from a conventional industrial lease.

In a warehouse lease, the primary issues may include rent, term, repairs, renewal options, operating expenses, and tenant improvements. In a port terminal lease, those same topics may also involve berth windows, crane availability, rail interface, yard density, gate operations, storm recovery, terminal operating systems, cybersecurity, decarbonization, grant-funded equipment, labor considerations, and political optics.

In other words, the lease is not just a document that grants occupancy. It is a framework for allocating operating control, infrastructure responsibility, capital risk, and public accountability.

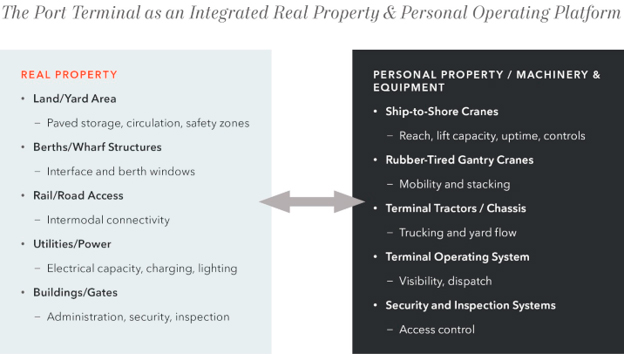

It helps to think of the negotiation in three layers. The first is real property: land, wharf, bulkhead, yard, buildings, pavement, utilities, access, and easements. The second is personal property and machinery and equipment: ship-to-shore cranes, rubber-tired gantry cranes, reach stackers, terminal tractors, chassis, scales, security equipment, lighting, reefer plugs, substations, charging infrastructure, and terminal operating systems. The third is public-policy risk: funding, labor, environmental compliance, community impact, and elected-official approval. A lease that addresses only the first layer can leave unaddressed the assets that actually move cargo, along with the public obligations attached to them.

Comparable rent is only useful when the comparison accounts for the rights and obligations attached to that rent. A terminal with reliable cranes, priority berth access, strong rail connectivity, sufficient electrical capacity, well-maintained pavement, and enforceable service-level commitments is not equivalent to a terminal where those items are uncertain, outdated, or controlled entirely by the port authority.

Why Machinery and Equipment Matter in Port Terminal Valuation

Port terminal economics often depend on the interaction between real property and personal property.

The real property provides the location, waterfront access, berth interface, yard, buildings, utilities, easements, and legal right to occupy. The personal property and machinery and equipment create much of the operating utility. A terminal without adequate cranes, terminal tractors, yard equipment, rail-loading infrastructure, power, software, and security systems may have land value, but limited operating value as a modern cargo platform.

This distinction is especially important in port terminal valuation, machinery and equipment valuation, lease advisory, financial reporting, lending, and public-sector capital planning.

Legal documents need to specify ownership, maintenance, replacement, access, priority use, insurance, casualty, removal rights, and end-of-term treatment. Financial reporting may require thoughtful treatment of real property improvements, leasehold improvements, machinery and equipment, depreciation, impairment, capital contributions, and useful life assumptions. Lenders and investors need to understand collateral beyond land and buildings. Public agencies need to evaluate whether a capital plan actually improves port capacity or merely shifts cost to the tenant.

In negotiation, the practical question is whether the rent structure reflects the entire operating platform. A tenant that funds and controls essential machinery and equipment may be delivering value beyond land rent. A port authority that owns and maintains reliable cranes, berths, rail, utilities, roads, and security infrastructure may support a stronger rent position.

Either way, the analysis should separate land scarcity from operating capability.

How Public Funding and Capital Investment Shape Port Lease Strategy

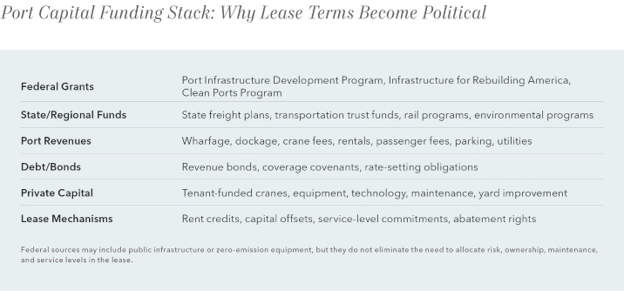

Port capital projects are rarely funded from a single source. Depending on the jurisdiction and project, funding may include federal grants, state transportation funds, local appropriations, port revenues, revenue bonds, tariff revenues, environmental programs, tenant contributions, private financing, or in-kind operating commitments.

Public funding can support major freight, safety, reliability, intermodal, environmental, and zero-emission infrastructure projects. However, funding alone does not answer the most important lease questions: who owns the asset, who controls its use, who maintains it, who benefits from it, and what happens if it does not perform as expected.

In practice, that funding flows through identifiable federal programs. The Maritime Administration’s Port Infrastructure Development Program funds berth, wharf, rail, and terminal improvements; the Nationally Significant Multimodal Freight and Highway Projects (INFRA) program supports freight, rail, water, port, and intermodal projects; and the Environmental Protection Agency’s Clean Ports Program has awarded nearly three billion dollars across more than fifty grants for zero-emission equipment and air-quality planning, drawing on multiyear funding under the Infrastructure Investment and Jobs Act. The existence of a program, however, does not resolve who owns, maintains, controls, schedules, or benefits from the resulting asset.

If a tenant contributes to cranes, electrical upgrades, terminal technology, yard improvements, rail enhancements, or emissions-reduction equipment, the lease should address how that investment is protected. Depending on the transaction, that may include rent credits, reimbursement rights, priority use, amortization protection, maintenance standards, extension options, termination compensation, or end-of-term rights.

From the port authority’s perspective, capital planning is also tied to public accountability. Bond covenants, grant conditions, procurement rules, environmental commitments, labor agreements, political approvals, and public-benefit narratives may limit what the port can offer. A rent concession may be difficult if the port needs revenue for debt service or future capital projects. A rent increase may be equally difficult if the infrastructure does not support the service levels required for higher throughput.

Why Competing Waterfront Uses Create Political Risk

Large port authorities often serve multiple constituencies at once.

Cargo operators need berth availability, cranes, truck gates, rail access, storage area, security lanes, and reliable maintenance. Cruise interests need passenger terminals, parking, baggage handling, security screening, berth priority, tourism infrastructure, and public-facing amenities. Recreational marine users may seek marina space, yacht services, boat repair, waterfront restaurants, dry storage, and public access. Nearby communities want jobs, cleaner air, reduced congestion, resilience, and protection from industrial externalities.

In major port markets such as Southern California, the South Atlantic, the New York/New Jersey harbor region, and the Pacific Northwest, these interests can compete for the same scarce resource: usable waterfront capacity.

A berth used for a cruise ship is not available for a cargo vessel at the same time. Land dedicated to passenger parking may not be available for container storage. Capital spent on public-facing improvements may not be available for cargo-yard modernization. Electrical capacity may need to be sequenced among shore power, charging infrastructure, cranes, refrigerated containers, lighting, and terminal equipment. Rail access, gate roads, bridge restrictions, and security zones can become practical constraints even where the port owns substantial acreage.

These uses can pull in different directions. Cargo operations are economically significant but often less visible to the public than cruise tourism or waterfront redevelopment. Cruise activity is more public-facing but draws on the same capital and berth capacity as freight. Recreational and waterfront uses may align with placemaking goals while being difficult to combine with heavy industrial cargo. Environmental and community groups may favor cleaner equipment and emissions reductions while also seeking to limit additional truck traffic. Labor interests may support investment that expands work while raising questions about automation, job classifications, and staffing. Because these priorities coexist on the same waterfront, lease terms are often shaped by how a port balances them.

For terminal operators, the practical lesson is clear: lease economics should be tied to the port authority’s actual operating commitments. If the port expects higher rent, longer-term tenant investment, or expanded throughput, the lease should address the infrastructure required to make those outcomes possible.

What Should Owner-Users and Terminal Operators Evaluate?

For an owner-user or terminal operator, the central issue is not simply whether waterfront land is scarce. It usually is. The more important issue is whether the leasehold, real property, machinery and equipment, and public infrastructure can support the business plan over the lease term.

Key questions include:

- Can the terminal handle the vessels expected to call?

- Are cranes large enough, reliable enough, and available during the right berth windows?

- Is the rail connection meaningful or merely nominal?

- Can the truck gate process volume without excessive dwell time?

- Is the pavement adequate for current container loads and stacking patterns?

- Does the electrical system support refrigerated containers, charging, lighting, security systems, and future equipment?

- Are maintenance obligations specific enough to avoid future disputes?

- If public infrastructure fails, what remedies does the operator have?

These questions matter because port terminals are throughput businesses. Small infrastructure constraints can create major operating consequences. A crane outage can delay a vessel. A berth conflict can push cargo to another port. A weak rail interface can shift containers to trucks, increasing cost and congestion. Insufficient yard capacity can create rehandling costs. Unclear maintenance obligations can turn public infrastructure into private operating risk.

A conventional rent study may not fully capture those issues unless the analysis connects rent to terminal functionality. The most relevant question is not simply, “What do other terminals pay?” It is, “What rights, infrastructure, equipment, obligations, term, risk allocation, and service levels were attached to those rents?”

Key Port Terminal Lease Terms to Review

Port terminal lease negotiations should evaluate more than base rent and term. Issues that often deserve closer attention include:

- Term and renewal options that align with the useful life and amortization period of major machinery and equipment investments

- Crane ownership, maintenance, uptime, modernization, replacement, priority use, and reimbursement rights

- Berth access, vessel-window coordination, wharf availability, and remedies for service failures

- Rail access, gate operations, road circulation, and intermodal connectivity

- Utility capacity, electrical upgrades, charging infrastructure, shore power, refrigerated container capacity, and energy-cost allocation

- Capital-offset structures, including rent credits, abatement, reimbursement, shared funding, priority rights, or extension options

- Environmental compliance and clean-equipment obligations, including grant-funded equipment, reporting, scrappage, and public-engagement requirements

- Technology and data systems, including terminal operating systems, cybersecurity, gate visibility, customer reporting, and access control

- Casualty, condemnation, resilience, storm recovery, and business-continuity obligations

- End-of-term treatment of tenant-funded improvements, machinery and equipment, removal obligations, and compensation rights

These terms are not merely legal details. They directly affect operating reliability, capital recovery, financing risk, customer commitments, and long-term asset value.

Who Needs Specialized Port Terminal Lease Advisory or Valuation Support?

Port terminal leases affect a wide range of stakeholders because they combine real estate, machinery and equipment, public infrastructure, capital planning, and operational risk.

For owner-users and terminal operators, the lease is a production document. It determines whether the terminal can support shipping-line relationships, cargo categories, customer commitments, labor scheduling, equipment replacement, maintenance planning, and business continuity. A rent number that ignores infrastructure constraints can quietly transfer public operating risk to the tenant.

For attorneys, the business terms need to be translated into enforceable lease language. Rights to use cranes, berths, rail, yard areas, technology, and utilities should be specific enough to avoid later disputes. If tenant capital is used to improve public-port assets, counsel should address ownership, reimbursement, default, remedies, casualty, public approvals, and end-of-term treatment.

For accountants and financial reporting teams, terminal leases may involve land, buildings, leasehold improvements, machinery and equipment, grant-funded assets, capital contributions, depreciation, useful lives, impairment considerations, and tax planning. The accounting outcome may differ materially depending on who owns the asset, who controls its use, who funds it, and who bears maintenance or replacement risk.

For lenders and investors, collateral risk depends on more than acreage. Buyer pool, renewal probability, operating control, equipment condition, lease term, capital needs, public funding, environmental obligations, and service-level rights all influence risk. Scarce waterfront land does not eliminate exposure if the operator lacks enforceable infrastructure rights.

For developers and public agencies, a port is not a blank redevelopment site. Maritime access, security rules, rail corridors, hazardous materials, storm exposure, environmental permits, dredging, labor, truck routing, and public-infrastructure obligations can constrain alternative uses. A speculative higher use may be politically visible but operationally unrealistic if it undermines cargo capacity, public revenue, jobs, or supply-chain resilience.

For communities and elected officials, the public interest is broader than rent maximization. Port decisions affect jobs, truck traffic, air quality, regional supply chains, tourism, public finance, and industrial land preservation. A sound lease negotiation should make those tradeoffs explicit rather than treating rent, capital, labor, emissions, and community impact as unrelated issues.

The Broader Lesson: Port Lease Economics Should Start with Operating Facts

A port terminal lease is a test of whether public infrastructure and private operating risk are aligned.

The visible real estate is only part of the story. The true operating platform is created by the combined performance of land, berths, cranes, rail, gates, utilities, equipment, labor, technology, capital, and governance.

When those elements work together, a terminal supports commerce, employment, tax base, and supply chain resilience. When they do not, the lease can become a rent dispute driven by an infrastructure problem.

The practical takeaway is that terminal lease negotiations should not start and end with comparable rent. They should begin with the operating facts: what the property must do, what infrastructure is required, who controls the machinery and equipment, who funds modernization, who maintains the assets, and who bears the risk if public infrastructure does not perform.

For questions about specialized asset valuation, port infrastructure, machinery and equipment, or complex owner-user real estate considerations, contact Daniel Boring, CRE®, MAI, ARA, ASA, Senior Vice President, Valuation Advisory Services.

Sources

- American Association of Port Authorities, “America’s Ports Economic Impact Study,” 2024. National jobs, gross domestic product, wages and benefits, and goods-value indicators.

- S. Department of Transportation, Maritime Administration, “MARAD By the Numbers,” accessed 2026. U.S. ports and daily cargo import tonnage.

- S. Department of Transportation, Maritime Administration, “Port Infrastructure Development Program,” 2026. Program purpose and Infrastructure Investment and Jobs Act funding.

- S. Environmental Protection Agency, “Clean Ports Program,” accessed 2026. Grant awards, zero-emission equipment and infrastructure, and air-quality and climate planning.

- S. Department of Transportation, “INFRA / Nationally Significant Multimodal Freight and Highway Projects,” 2025. Freight, rail, water/port, and intermodal eligibility.

- Bureau of Transportation Statistics, “Port Performance Freight Statistics Program,” 2026. Nationally consistent port capacity and throughput measures.

- IBISWorld, “Ocean & Coastal Transportation in the US,” 2026. Industry revenue, employment, and trend context.

- IBISWorld, “Port & Harbor Operations in the US,” 2026. Industry risk, infrastructure quality, competition, and operating-risk context.

Frequently Asked Questions About Port Terminal Lease Negotiations

What should be considered in a port terminal lease negotiation?

A port terminal lease should evaluate rent, term, berth access, crane availability, rail connectivity, utility capacity, gate operations, maintenance obligations, machinery and equipment ownership, public funding requirements, environmental obligations, and remedies if infrastructure does not perform.

Why are port terminal leases different from conventional industrial leases?

Port terminal leases depend on a broader operating platform that includes public infrastructure, personal property, machinery and equipment, labor, technology, environmental compliance, and capital planning. The lease must address how those elements support cargo movement and long-term operating reliability.

How does public infrastructure affect port terminal lease economics?

Public infrastructure affects lease economics because the terminal operator’s ability to generate throughput may depend on assets controlled by the port authority, including berths, cranes, rail access, utilities, roads, security infrastructure, and capital improvement schedules.

Why should machinery and equipment be evaluated in a port terminal lease?

Machinery and equipment often create much of a terminal’s operating utility. Cranes, terminal tractors, reach stackers, yard equipment, charging infrastructure, security systems, and terminal operating technology can materially affect value, risk, and lease economics.

Who needs specialized port terminal valuation or advisory support?

Owner-users, terminal operators, attorneys, accountants, lenders, investors, public agencies, and port authorities may need specialized valuation or advisory support when lease economics depend on infrastructure performance, tenant-funded capital, machinery and equipment, or public-private risk allocation.

Disclaimer: Case details, figures, ownership information, and property identifiers have been modified or generalized to protect confidentiality. This article is based on real-world appraisal and advisory experience and is presented for educational purposes only. It is not intended as valuation advice, legal advice, engineering advice, environmental advice, transportation planning advice, or investment advice for any specific property, transaction, lease negotiation, or dispute.

Contact

Daniel Boring, , CRE®, MAI, ARA, ASA, Senior Vice President, Valuation Advisory Services

Stay in the know and subscribe to our monthly Western U.S. Market Trends report and our quarterly market research.